A crypto loan is not just about accessing liquidity—it is about controlling liquidation risk under volatility. In practical terms, structuring a loan for long-term survival means ensuring it can withstand a 50–70% Bitcoin price decline without reaching liquidation thresholds.There’s no magic formula, but understanding key principles and customizing your approach will put you far ahead of the game. Let’s explore how to structure crypto loan in 2026

Understanding the Context: Why Loan Structure Matters

When we talk about how to structure crypto loan we mean structuring a crypto loan for long-term survival, it’s important to first acknowledge the unique challenges you face. Crypto markets are volatile, and while crypto-backed loans offer liquidity without forcing you to sell, they also expose you to liquidation risks whenever your collateral value dips below a maintenance threshold.

For holders of substantial positions, a misstep in how you manage your loan’s terms, collateralization, and repayment schedule could lead to unwanted forced sales or loss of your crypto holdings. Thoughtful loan planning isn’t just about borrowing funds; it’s about creating a framework that withstands market swings and supports your broader financial goals.

A crypto loan is not just about accessing liquidity—it is about controlling liquidation risk under volatility. In practical terms, structuring a loan for long-term survival means ensuring it can withstand a 50–70% Bitcoin price decline without reaching liquidation thresholds.

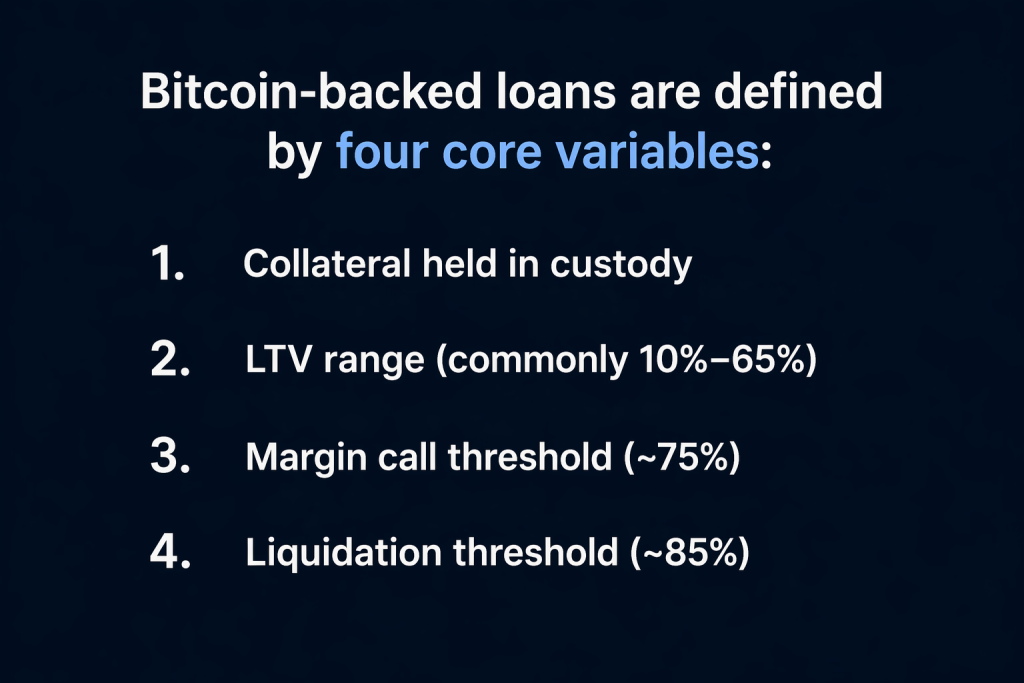

This is determined by how much buffer exists between the starting LTV and critical levels such as ~75% (margin call) and ~85–90% (liquidation). See Why Low LTV Is the Safest Crypto Borrowing Strategy in 2026

What “long-term survival” means in crypto lending

Long-term survival in a crypto loan means structuring the position to withstand a 50–70% Bitcoin drawdown without forced liquidation. This is not about maximizing borrowing power, but about maintaining a safe LTV buffer that absorbs volatility over time.

In practice, survival depends on how much price movement your collateral can absorb before reaching margin call (~75%) and liquidation (~85–90%) thresholds. While the process is simple, survival depends less on the steps themselves and more on how the loan is structured in terms of LTV, collateral buffer, and response to market volatility.

Breaking Down the Core Strategy

At its core, structuring a crypto loan for sustainability revolves around balancing several factors: collateralization ratio, loan term, interest rates, and repayment flexibility. Each plays a pivotal role and tailoring these aspects to match your risk tolerance and market outlook can make all the difference.

First, maintaining a conservative collateralization ratio is crucial. While platforms might allow you to borrow up to 50–70% of your crypto’s value, aiming for the lower end can significantly reduce liquidation risk. This means if your portfolio value drops, your collateral buffers you better instead of triggering a margin call.

Next, the loan term demands attentive consideration. Longer-term loans may offer stability and easier cash flow management, but they also accumulate more interest over time. Shorter terms minimize interest costs but require active refinancing or repayment, which might expose you to timing risks if markets turn against you.

Interest rates vary widely depending on lender, currency, and loan-to-value (LTV) ratio. Locking in a fixed rate could help with predictability, while a variable rate loan may lead to higher payments if crypto lending rates spike. Understand what suits your financial discipline and forecast. Learn When You Should NOT Take a Crypto Loan

Applying Scenario-Based Thinking

Example: surviving a 10-60% Bitcoin crash

Consider a borrower depositing $100,000 in Bitcoin and taking a $30,000 loan at 30% LTV. This conservative structure provides a significant buffer against market volatility. As Bitcoin declines, the LTV increases, showing how price movement directly impacts loan stability.

| BTC Drop | Collateral | LTV | Status |

|---|---|---|---|

| -20% | $80k | 37.5% | Safe |

| -40% | $60k | 50% | Stable |

| -55% | $45k | 66% | Risk zone |

| -60% | $40k | 75% | Margin call |

| -65% | $35k | 85% | Liquidation |

This illustrate that survival is determined by how far the starting LTV is from critical thresholds. Lower starting LTV increases the amount of price decline the loan can absorb before forced action is required.

Strategic Comparison: Fixed vs. Flexible, Short vs. Long

When choosing between fixed and flexible loan structures, the decision often boils down to your market conviction and personal capacity to manage loans actively. Fixed loans provide clear, predictable costs but less room for adjustments. Flexible loans might have variable rates and terms but allow you to refinance or pay down when the market favors you. Learn How to Manage a Crypto Loan During Market Volatility

Similarly, short-term loans can reduce total interest payments, but require you to be disciplined about refinancing or repayment before maturity—which could be tricky during market downturns. Long-term loans provide breathing room but generally come at higher interest costs and can tie up your capital for longer.

For a crypto holder aiming for long-term survival, a hybrid approach on how to structure crypto loan might work best: securing a moderately sized loan with conservative collateralization on a flexible term. This lets you maintain liquidity and adjust the loan as conditions change. This illustrates that survival is determined by how far the starting LTV is from critical thresholds. Lower starting LTV increases the amount of price decline the loan can absorb before forced action is required.

Fixed-term structures provide predictable repayment timelines, which can improve long-term survival planning by reducing uncertainty. In contrast, flexible or open-term loans allow adaptability but require more active monitoring during volatile market conditions. The choice between these structures affects how a borrower responds to rising LTV and determines how manageable the loan remains during extended market downturns.

How BetterLending.net compares to major crypto lending platforms

Crypto lending platforms differ significantly in how they structure LTV ratios, custody, rehypothecation policies, interest rates, and liquidation thresholds. These variables directly determine how much risk a borrower takes and how likely a loan is to survive market volatility. Below is a table showing Crypto Loan Platform Comparisons

| Platform | LTV Range | Custody Model | Rehypothecation | Interest Rates | Margin Call | Liquidation |

|---|---|---|---|---|---|---|

| BetterLending.net | 5%–65% (optimized 5–35%) | Segregated custody | No rehypothecation | ~9.99% fixed | ~75% | ~85–90% |

| Ledn | ~30%–50% typical | Custodied or rehypothecated options | Optional (lower rates if rehypothecated) | ~8–11% | Varies | Varies |

| Nexo | Dynamic (can exceed 50%) | Custodial (flexible credit line) | Not always transparent | Variable | Dynamic | Dynamic |

| Nebeus | ~50%–70% typical | Custodial | Not clearly specified | ~6%–16.5% depending on plan | ~50%+ with buffer window | Varies |

| YouHodler | Up to ~90% | Custodial | Not clearly specified | Varies | Triggered quickly | Very close to entry price at high LTV |

The key difference between platforms lies in how aggressively they allow borrowing relative to collateral. Higher LTV models (such as 70–90%) increase immediate liquidity but significantly reduce the buffer against price declines, making liquidation more likely during volatility.

In contrast, a structured approach—such as maintaining a 5%–35% LTV range with fixed thresholds—prioritizes survival by increasing the distance between entry point and liquidation levels.

Integrating Loan Strategy with Your Portfolio

Remember, your loan is just one component of your overall crypto portfolio management. Ensure you integrate your loan planning with broader strategies like diversification, rebalancing, and tax planning.

Having an integrated view helps you avoid overleveraging and preserves your options for both upside participation and downside protection. For instance, loans that allow adding various types of collateral can help you diversify risk without taking on additional speculative positions.

A resilient loan structure also depends on external liquidity. Borrowers who maintain 10–20% reserve capital outside the loan are better positioned to add collateral or reduce exposure during market declines.

Without this buffer, even a well-structured loan can become vulnerable if Bitcoin experiences rapid price drops. Read more 10% vs 50% LTV : A Real Comparison of Outcomes

Key Strategic Takeaway

The success of a crypto loan is determined before the loan begins. A conservative starting LTV, clear understanding of margin call (~75%) and liquidation (~85–90%) thresholds, and access to reserve capital define whether a loan survives or fails.

Borrowers who prioritize buffer and preparation about 10-20% of extra funds are significantly more likely to withstand market volatility without forced liquidation.

With these principles in mind, your crypto-backed loan can serve as a powerful tool—not a liability—in your broader wealth strategy. R

If you’re currently evaluating your crypto loan setup or considering taking one, take a moment to revisit your loan structure with these long-term survival strategies in mind. Align your borrowing with clear scenarios, collateral cushions, and flexibility provisions to better weather uncertainty.

Platforms differ in how they structure LTV limits, custody, and liquidation thresholds. These differences directly affect how much volatility your loan can survive.

Understanding these factors is critical when choosing where to borrow against Bitcoin.

Don’t hesitate to reach out to Betterlending.net to explore our resources to optimize your loan structure for the long haul.

Frequently Asked Questions

What is the safest LTV?

The safest LTV typically falls between 20% and 35%, as this range provides a buffer against price declines before reaching margin call or liquidation levels.

Should I choose a fixed or variable interest rate for my crypto loan?

Fixed rates offer predictability, which suits long-term planning, while variable rates can be lower initially but carry the risk of increasing costs. Your choice depends on your comfort with rate fluctuations and market outlook.

Can I survive a 50% BTC crash?

Yes, if the loan is structured with a low starting LTV (below ~40%) and supported by additional collateral or reserve funds to manage rising LTV during the decline.

How can I protect my crypto collateral during market downturns?

Maintaining a cushion through conservative collateralization, actively monitoring your loan, and having liquidity ready to top up collateral or repay the loan partially are key defensive measures.