In the evolving world of crypto-backed lending, deciding on the right loan-to-value (LTV) ratio is more than just a calculation — it’s a strategic choice that can shape your financial flexibility and risk exposure. For crypto holders with sizable positions, particularly those managing portfolios north of $50,000, the question often boils down to this: which one between 10% vs 50% Ltv implies a smarter move? This week, we dive into the real outcomes behind these two scenarios, unpacking what each means for your portfolio resilience, costs, and

peace of mind.

Understanding the Strategy Context

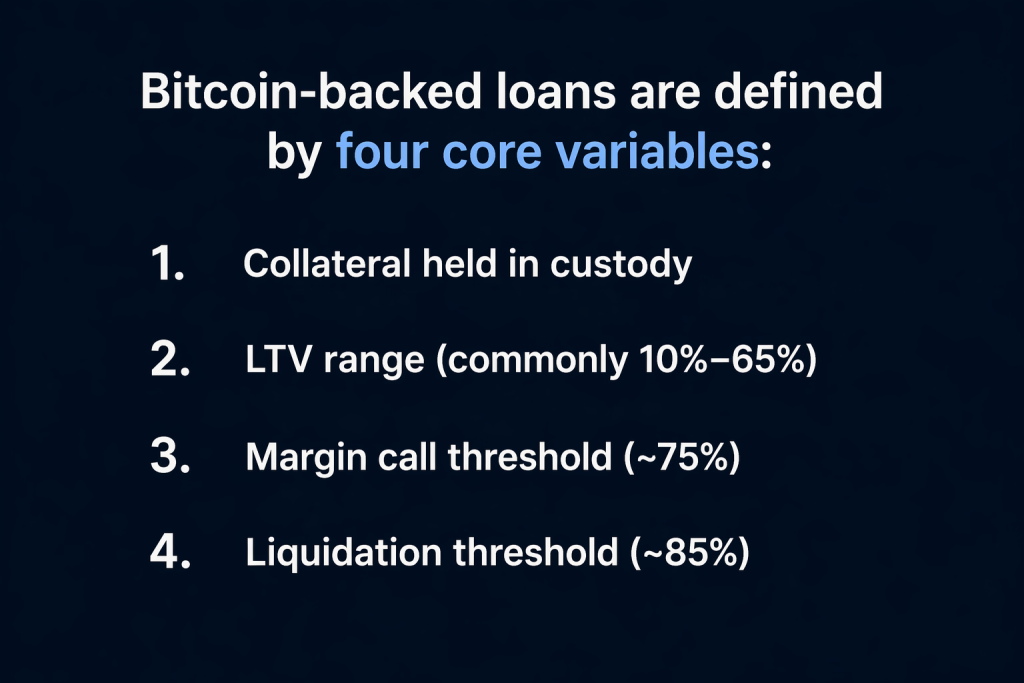

LTV ratio defines the portion of your crypto collateral you are borrowing against. A 10% vs 50% LTV means how much you can borrow against a a fraction of your holdings’ value, while 50% represents a much larger loan relative to collateral size. At first glance, the appeal of borrowing more is obvious—you access greater liquidity without selling assets, potentially keeping your position intact for future gains. However, higher leverage also increases the risk of liquidation if market conditions turn sour.

Conversely, a lower LTV reduces that risk but limits your immediate capital. This trade-off isn’t theoretical—it plays out in the day-to-day management of your portfolio and your ability to navigate volatility without stress or forced sales. Smart crypto loan strategies

Breaking Down the Core Strategies

Let’s start with a 10% LTV loan. By borrowing conservatively, you maintain a significant equity buffer between the loan value and your collateral. This buffer provides a cushion against price swings, meaning that even during market dips, your loan remains well-collateralized and your risk of liquidation low.

In contrast, a 50% LTV loan places you much closer to the liquidation threshold. While you enjoy access to more capital—for say, investments, expenses, or other opportunities—the margin for error shrinks dramatically. Market volatility that your portfolio could otherwise weather comfortably at 10% LTV may trigger margin calls or liquidations at 50%, especially in sharp downturns.

Scenario-Based Thinking: Looking at Volatility Through the Lens of LTV

Imagine you hold $100,000 in collateral. Borrowing $10,000 at 10% LTV offers you liquidity while keeping your leverage conservative. Price drops of up to 20%-30% in your collateral won’t immediately risk your loan’s health. You can breathe easier, knowing that the platform’s liquidation mechanics won’t spring into action overnight.

Now, consider taking a $50,000 loan at 50% LTV. The same price drop could trigger rapid liquidations, especially since collateral value and loan value are much more tightly coupled. Sudden market corrections can erode your collateral value to the point where it no longer sufficiently backs the loan. Liquidation events become more frequent and detrimental, potentially wiping out portions of your crypto holdings.

Strategic Comparison: Beyond Just Risk

Risk is the headline, but there’s nuance beneath the surface. Higher LTV loans typically come with higher interest rates or fees, reflecting the increased risk lenders assume. This means your borrowing costs may compound over time. Meanwhile, lower LTV loans tend to have more favorable rates, letting you hold onto collateral longer and benefit if market conditions recover.

Liquidity needs must also be factored in. If your capital usage is short-term and you expect rapid repositioning, a higher LTV loan may deliver the immediate cash you need. For longer-term holders seeking to mitigate risk and avoid forced sales, conservative borrowing aligns better with that goal.

Another consideration is your comfort with actively managing your positions. Higher leverage demands close monitoring and readiness to respond to margin calls. Lower leverage gives you wider margins of safety and reduces the emotional wear of market swings.

Contextualizing Your Loan Decision

At BetterLending, we’ve seen firsthand how loan terms and user outcomes vary wildly depending on chosen LTV levels. For further insights on managing loan health during volatility, see our guide on “Managing Crypto Loans Through Market Swings”. For a detailed breakdown of fees and how they affect long-term loan profitability, explore our “Interest and Fees Explained” resource page.

Key Strategic Takeaway

Choosing between a 10% and a 50% LTV comes down to balancing your appetite for liquidity against your tolerance for risk and active management. The safer path of 10% LTV gives ample room to absorb market fluctuations without jeopardizing your collateral. The more aggressive 50% LTV loan may unlock more capital today but increases the chances of painful liquidations and higher cumulative borrowing costs.

For crypto holders with serious stacks, this isn’t just about numbers—it’s about aligning your borrowing strategy with your overall portfolio philosophy, risk capacity, and market outlook.

Assess your current portfolio and consider where you stand on this trade-off. Whether you lean towards conservative borrowing or calculated leverage, having a clear understanding of how your LTV choice affects your outcomes is essential. BetterLending is here to provide tools and transparency that help you make those decisions more confidently.

Stay tuned next week when we’ll dive into advanced loan management techniques to optimize borrowing costs while minimizing liquidation risk. Until then, approach your crypto-backed loans with clarity—your strategy today shapes your financial freedom tomorrow.

Frequently Asked Questions

What factors should influence my choice of LTV ratio?

Consider your risk tolerance, the volatility profile of your collateral, liquidity needs, and your ability to actively manage margin calls. The broader market environment and interest rates also play important roles.

Can I adjust my LTV after taking out a loan?

Many platforms, including BetterLending, allow you to repay part of the loan or add more collateral, effectively lowering your LTV. This flexibility helps manage risk as market conditions change.

Does a lower LTV always mean lower interest rates?

Generally, yes. Lower LTV loans imply reduced risk for lenders, which often translates into better rates. However, other factors like loan duration and market conditions also influence interest costs.

What happens if my collateral value drops below the loan value?

This triggers margin calls and potentially liquidation, where part or all of your collateral is sold to cover the loan. The closer your LTV is to the maximum allowed, the quicker liquidation can occur during price downturns.

Is it better to borrow more or keep loans small if I plan to HODL long term?

If your goal is long-term holding, lower LTV borrowing usually offers more security and less risk of forced liquidation. Large loans at high LTV levels pose greater risk, especially in volatile markets.