For some one to sufessfully Manage a crypto loan during volatility requires continuous monitoring of LTV rather than price alone. A falling market does not automatically cause liquidation, but it accelerates LTV expansion toward critical thresholds.

The key is to know how to Manage a crypto loan , track how quickly LTV is rising and act before it reaches margin call levels, rather than reacting after alerts are triggered.

In the fast-paced world of cryptocurrency, volatility isn’t just common — it’s expected. For a crypto holder with a sizable position, navigating the unpredictable swings of the market gets even trickier once loans are in play. Knowing how to Manage a crypto loan during these ups and downs calls for more than just reactive moves. It demands a blend of strategic foresight, calm assessment, and practical action. Learn How to Structure Crypto Loan for Long-Term Survival in 2026

Understanding the Strategy Context

Crypto loans aren’t your typical financial instruments. They’re uniquely tied to the underlying asset’s price, which means every market dip or spike directly influences your loan position. For a holder with $50K or more in crypto, to manage a crypto loan relationship becomes a critical factor in both risk management and opportunity.

Traditional loans rely on fixed collateral values or stable assets, but in crypto lending, collateral value oscillates widely — sometimes within minutes. This means standard loan-to-value (LTV) ratios require constant monitoring to avoid margin calls or forced liquidation. Recognizing this volatility as a foundational factor changes how one approaches loan management.

Managing a crypto loan during volatility is not about predicting the market, but about controlling how rising LTV affects liquidation risk.

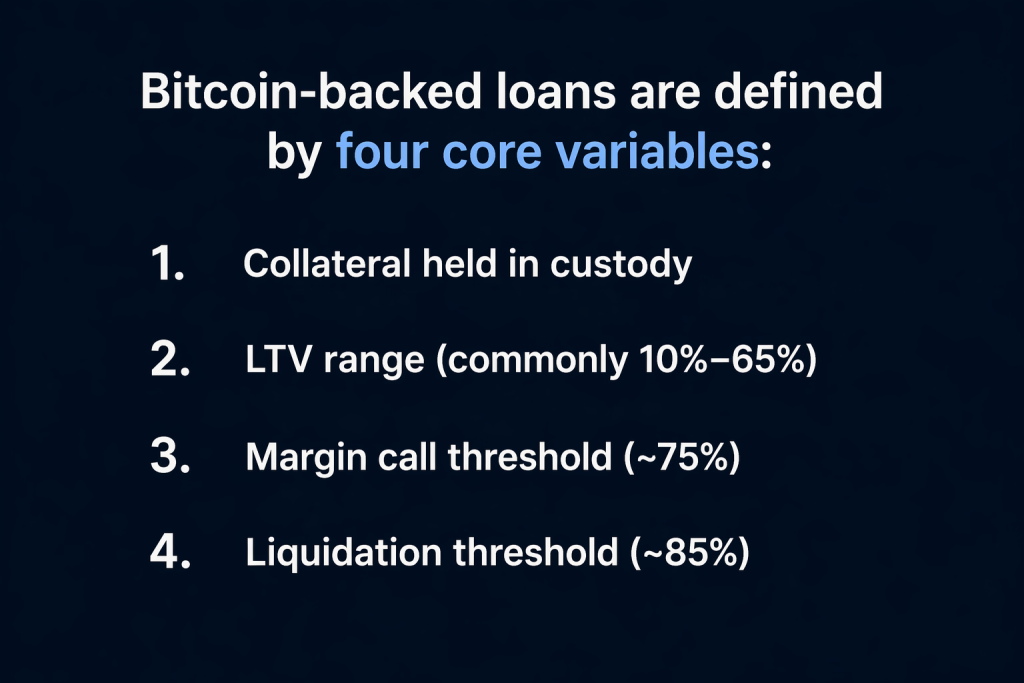

In practice, a loan becomes dangerous not when prices fall, but when the LTV approaches ~75% (margin call) and ~85–90% (liquidation) thresholds.

Breaking Down Core Strategies for Loan Management

Effective crypto loan management starts with a few core principles tailored for fluctuating markets. First, setting a conservative LTV is vital. While borrowing against 70% or more of your collateral might seem appealing, a buffer zone (say, aiming lower around 50-60%) helps absorb sudden market shocks.

Second, regularly monitoring your loan health metrics — especially collateral value and LTV — isn’t optional. Automated alerts can aid in this, but manual checks and market watchfulness still matter immensely. Preparing to act swiftly stops small issues from snowballing.

Third, consider structured repayment plans or partial loan paydowns during bullish periods. Reducing your exposure before volatility spikes can prevent distress during downturns.

Lastly, stay informed about your loan provider’s specific margin call policies and liquidation thresholds. Each platform has nuances that affect how and when you need to respond.

Scenario-Based Thinking: Preparing for Market Swings

Situational planning is crucial when market swings are the norm. Imagine a scenario where your $50K crypto collateral suddenly drops 30% in value. If your loan was initially set at 60% LTV, this dip could push you perilously close to a margin call.

Having scenario plans means you’re not scrambling. This could involve pre-arranged access to additional collateral to top up your loan, setting aside fiat reserves to pay down the loan quickly, or having triggers in place for automatic loan rebalancing services if available.

On the flip side, if the market rallies, think about tapping into that extra collateral value judiciously. Reinvesting borrowed funds or increasing loan size requires fresh calculations and a clear understanding of risk tolerance. Learn Why Low LTV Is the Safest Crypto Borrowing Strategy in 2026

Comparing Approaches: Passive vs. Active Loan Management

At a high level, crypto borrowers fall into two camps. Passive managers take a set-it-and-monitor approach, relying mostly on alerts and reserves. Active managers engage continuously — adjusting collateral, shifting repayment schedules, or tweaking loan amounts in real time.

Each has trade-offs. Passive management can work well if you maintain a substantial safety buffer and longer time horizons. However, in volatile phases, active management offers more adaptability but requires tighter discipline and time commitment.

In early-stage volatility, where LTV remains below 50–60%, no immediate action is required beyond monitoring. As LTV approaches 65–75%, the loan enters a defensive phase, where adding collateral or partial repayment becomes necessary.

Once LTV moves beyond ~75%, the borrower is no longer managing risk but reacting to it, as margin calls indicate the buffer has largely been exhausted.

The Difference Between Aggressive vs conservative crypto borrowing in 2026

Choosing your style depends on your capacity to track markets, your liquidity at hand, and psychological comfort with risk. Experimentation with a smaller tranche of your holdings before scaling up can help identify what fits best.

Why Ongoing Education Matters

BetterLending’s knowledge hub offers continuous updates on loan management best practices, market insights, and product features that can amplify your loan strategy. Staying connected to expert analyses and evolving tools reinforces your ability to respond decisively when volatility strikes.

Additionally, exploring case studies from seasoned crypto borrowers can shed light on effective strategies others have used to protect their assets and minimize unnecessary liquidation risk during downturns.

Crypto lending platforms like nebeus, nexo and Ledn and Betterlending.net use automated systems to protect against losses. When LTV reaches predefined thresholds, margin calls are triggered, and if conditions worsen, collateral may be liquidated automatically.

These systems operate in real time, meaning delays in response can result in forced liquidation even during short periods of market volatility.

Key Strategic Takeaway

At the heart of managing crypto loans through volatile markets lies a mindset of preparedness and measured adaptability. Overleveraging in a high-volatility environment often leads to pressure points that are tough to unwind. Instead, prioritizing conservative loan terms, active monitoring, and scenario planning can empower you to retain control and capitalize on market movements without unwanted surprises.

Leveraging a crypto loan should feel like a calculated tool, not a gamble on price swings. With disciplined management, loans become a strategic asset that can enhance portfolio flexibility rather than jeopardize it.

Take a moment to review your current loan positions or lending plans with the lens of volatility management. Are your LTV ratios conservative enough? Do you have clear strategies in place for rapid market changes? If these questions spark new ideas or concerns, consider diving deeper into BetterLending’s resources or reaching out to our team for tailored advice.

Effective volatility management depends on preparation before market stress occurs. Borrowers who maintain additional liquidity can respond by adding collateral or reducing exposure as LTV rises.

Without this preparation, even a well-structured loan can become vulnerable if market declines occur rapidly.

Managing a crypto loan during volatility is not about avoiding price drops, but about ensuring the loan can withstand them. The ability to survive depends on how much buffer exists between the starting LTV and liquidation thresholds.

Borrowers who understand and manage this relationship can navigate volatility, while those who ignore it are more likely to face forced liquidation.

Frequently Asked Questions

How often should I monitor my crypto loan during volatile market conditions?

Monitoring frequency depends on the volatility level. During extreme swings, daily checks or automated alerts are recommended. In calmer times, weekly reviews might suffice, but always stay prepared for sudden changes.

What’s the safest loan-to-value (LTV) ratio to maintain in a volatile market?

Maintaining an LTV between 50-60% provides a robust buffer against price drops. This range strikes a balance, minimizing liquidation risk while allowing you to leverage your assets efficiently.

Can I add more collateral after taking a crypto loan to avoid liquidation?

Yes, adding collateral is a common strategy to strengthen your loan position and reduce margin call risk, especially during downturns. Ensure your lending platform supports this feature and understand the process to execute it swiftly.

What happens if my loan undergoes liquidation?

If your collateral value falls below the required threshold and you don’t act, the lender may liquidate part or all of your collateral to cover the loan. This usually locks in losses and ends your loan agreement.

Are there tools to automate loan management during volatile markets?

Certain platforms offer automated monitoring, alerts, and even dynamic loan adjustments. While useful, it’s wise to complement these tools with your own oversight and a clear action plan.