The custodial vs non-custodial distinction is not a product preference — it is a structural risk decision. In a custodial loan, the platform holds the private keys and can liquidate automatically at the threshold LTV, typically 83–90%, without borrower approval. In a non-custodial model, liquidation requires multi-party signature coordination — which introduces delays that most capital providers will not accept at scale. The choice between the two determines not just how the loan operates, but how many independent ways it can fail. Learn more; Crypto Collateral & Custody: The Complete Risk Framework for Borrowers (2026 Guide)

Custody Is Not Just Storage — It Is Liquidation Authority

Understanding the custodial vs non-custodial structure of a crypto-backed loan starts with a single mechanic: when BTC or ETH is sent to a lending platform as collateral, the borrower transfers not just the asset — but the right to liquidate it. Custody determines control, and control determines who executes the liquidation when LTV thresholds are breached. This is the mechanism most borrowers misread as an administrative detail and most competitor articles fail to explain.

In a fully custodial loan, the platform controls the private keys from deposit to repayment. At 75–80% LTV, a margin call is issued. At 83–90% LTV, the platform executes liquidation without any further action from the borrower. The process is automated, immediate, and does not wait for the borrower to respond, confirm, or intervene. The borrower’s ability to save the position ends at the margin call — not at liquidation.

The custodial vs non-custodial choice also determines who funds the loan at scale. Without unilateral liquidation authority, the capital provider — the entity actually providing the USD — cannot guarantee recovery. That constraint is what makes non-custodial loan models structurally limited to peer-to-peer arrangements at small volumes, and why they are not available as standard retail products from regulated lenders.

For a detailed breakdown of how LTV thresholds and liquidation mechanics interact, see BetterLending’s guide on crypto loan liquidation mechanics.

What Actually Happens After the Borrower Sends Collateral

The deposit transaction is the start of a sequence most borrowers do not fully map before committing capital. Each step has a corresponding risk implication that differs depending on whether the loan is custodial or non-custodial:

Step 1: Private Key Transfer

The borrower sends collateral to a platform-controlled wallet address. The private keys to that wallet belong to the platform — or the platform’s designated custodian. From this point forward, the borrower has a contractual claim on the collateral, not a direct cryptographic one. The distinction matters: a contractual claim is enforced through legal process; a cryptographic claim is enforced on-chain, without intermediaries.

Step 2: Collateral Locking and LTV Initialisation

The platform calculates the starting LTV — (loan balance ÷ collateral value) × 100 — and begins monitoring it in real time. A $50,000 loan against 1 BTC at $90,000 initialises at 55.5% LTV. The platform’s risk engine begins tracking the position against the margin call threshold (typically 75–80%) and liquidation threshold (typically 83–90%) from the moment the collateral is confirmed on-chain.

Step 3: Continuous LTV Monitoring

Price feeds update the LTV calculation on a continuous basis — not daily, not hourly. A 20% BTC price drop from $90,000 to $72,000 pushes LTV from 55.5% to 69.4% in real time. The platform’s margin call system triggers automatically when the threshold is crossed, regardless of the time of day or whether the borrower is actively monitoring the position.

Step 4: Margin Call Notification

At the margin call threshold — typically 75–80% LTV — the platform issues a formal notification. The borrower can respond by adding collateral to lower LTV, repaying partial principal, or closing the position. The window between the margin call and liquidation execution varies by platform: BetterLending provides a defined notification window; automated platforms like Nexo and YouHodler may proceed to execution within hours.

Step 5: Liquidation Execution

At the liquidation threshold — typically 83–90% LTV — the platform sells enough collateral to bring the loan back to target LTV, or closes the position entirely. Because the platform controls the private keys in a custodial structure, this execution requires no borrower action or approval. The sale occurs at market price at the moment of execution — not the price at the time of the margin call — which in a fast-moving market can be materially worse.

Custodial vs Non-Custodial: Segregated vs Pooled — Why the Distinction Is Material

Not all custodial models carry equivalent risk. The critical structural variable is segregation — whether each borrower’s collateral is held in a dedicated account isolated from platform operations and other borrowers’ assets, or whether it is pooled into a co-mingled structure that the platform manages as a single block.

In a segregated custody model, the borrower’s collateral occupies its own on-chain address or custodial account. It is legally ring-fenced from the platform’s operational funds, other borrowers’ collateral, and any lending or yield activity the platform engages in. If the platform becomes insolvent, a segregated structure means the collateral is identifiable and legally protected — not treated as part of the general estate available to unsecured creditors.

In a pooled model, all borrower collateral sits in accounts the platform controls as a single operational pool. Individual borrowers have no on-chain visibility into their specific collateral. In an insolvency scenario, that pool becomes part of the bankruptcy estate, and individual borrowers must make claims through legal proceedings rather than recovering assets directly. This is the structure that turned the 2022 lender collapses into multi-year recovery processes for thousands of borrowers.

BetterLending maintains segregated custody across all loan products. Collateral is held in a designated custody arrangement that is separate from platform operational funds, not co-mingled with other borrowers’ assets, and not exposed to the platform’s other financial activities.

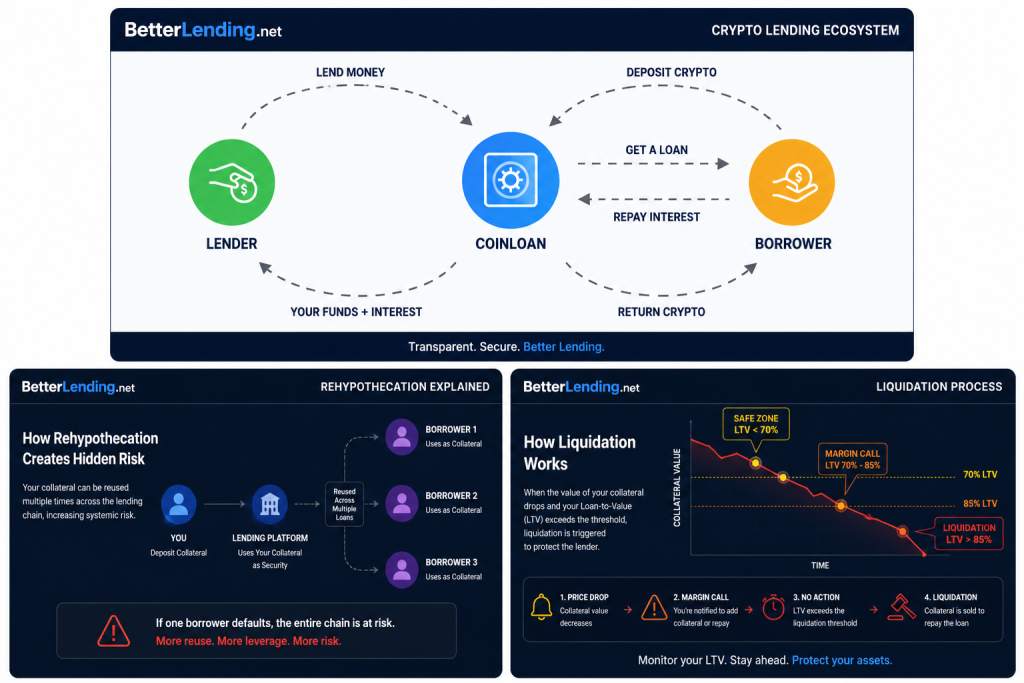

Rehypothecation: The Second Risk Layer Inside Custodial Models

Within the custodial vs non-custodial decision sits a further structural variable that determines the real risk profile: whether the platform rehypothecates the collateral — reusing it for lending, staking, or yield activities — or holds it exclusively against the borrower’s loan.

Rehypothecation introduces a second layer of risk beyond price volatility. The collateral is now simultaneously securing the borrower’s loan and exposed to whatever the platform has done with it downstream. If a third party holding rehypothecated collateral becomes insolvent, the borrower’s position is impacted by a failure that has no relationship to BTC price, LTV, or anything within the borrower’s control.

The platforms that collapsed in 2022 — Celsius and others — were not simply victims of bad market conditions. Their structures allowed, and in some cases required, rehypothecation across multiple counterparty layers. When market stress hit, the chains broke simultaneously, and borrowers discovered their collateral was inaccessible before liquidation could even be executed. For context on how rehypothecation operates and what to verify before depositing collateral, see BetterLending’s guide on what is rehypothecation and why it matters.

Stress Scenario: A 40% BTC Drop Across Two Different Custody Structures

Starting Conditions (Both Scenarios)

- Collateral: 1 BTC at $90,000

- Loan: $50,000 | Entry LTV: 55.5%

- Margin call threshold: 78% LTV

- Liquidation threshold: 88% LTV

Scenario A — Custodial vs Non-Custodial: Segregated, No Rehypothecation

BTC drops 25% → $67,500 | LTV: 74%

Below margin call. Borrower receives no notification. Adding $10,000 collateral drops LTV to ~63% — buffer restored.

BTC drops 40% → $54,000 | LTV: 92.5%

Liquidation threshold breached. Platform sells collateral. Borrower receives $54,000 minus $50,000 loan minus fees. Collateral was segregated — no additional custody failure.

Scenario B: Pooled Custody, Rehypothecation Active

BTC drops 25% → $67,500 | LTV: 74%

LTV within bounds. But the platform’s rehypothecation counterparty is also facing margin calls on unrelated positions — beginning to restrict collateral access.

BTC drops 40% → $54,000 | LTV: 92.5%

Liquidation threshold breached. Platform attempts to liquidate — but rehypothecated collateral is frozen at the third party. Liquidation cannot execute. Platform suspends withdrawals. Borrower is now an unsecured creditor in bankruptcy proceedings, with no timeline or guaranteed recovery amount.

The market event was identical in both cases. The custodial vs non-custodial and segregation decisions — made at the time of deposit — determined the outcome entirely. The LTV ratio and price movement were the same; the structural conditions were not.

Decision Framework: What LTV Level Requires Action

- Below 60% LTV: No action. Monitor weekly.

- 60–65% LTV: Personal threshold. Add collateral or reduce principal. Do not wait for margin call.

- 65–78% LTV: High urgency. Deploy reserve liquidity within hours.

- Above 78% LTV: Margin call issued. Liquidation clock is running.

Custodial vs Non-Custodial: How BetterLendingnet, Ledn, Nexo, Nebeus and YouHodler Compare

BetterLendingnet operates fully segregated custody across all loan products. Collateral is held against the borrower’s specific loan, not pooled. Rehypothecation is prohibited. Liquidation occurs through a structured margin call process with a defined notification window — not an automated engine that executes at threshold without delay. Entry LTV defaults are designed to preserve a 30–35% price decline buffer before the margin call level is reached.

Ledn has moved to a fully custodied BTC-only model as of mid-2025, eliminating its Standard Loan product that previously involved rehypothecation. All collateral is now held in segregated, on-chain verifiable addresses, ring-fenced from funding partner assets. Ledn’s LTV cap of 50% for BTC loans is the most conservative in the retail market — it limits accessible capital but provides the widest survival buffer. Bi-annual proof-of-reserves attestations provide transparency, but the 6-month cycle means real-time collateral verification is not available.

Nexo operates in-house custody with insurance coverage, but the insurance policy limits, eligible events, and sub-limits require direct verification before committing collateral above $50,000. Dynamic LTV adjustments tied to NEXO token holdings introduce a variable that does not exist in BTC or ETH-only structures — NEXO price movement can affect the effective LTV calculation in ways that are not visible on a standard loan dashboard. Liquidation is fully automated with limited human intervention.

Nebeus offers fixed-term loan structures that remove some real-time liquidation pressure by fixing loan terms at origination. The tradeoff is flexibility: fixed terms limit the ability to repay early or restructure the position if market conditions change. Custody and rehypothecation terms require direct confirmation from the platform — fixed terms do not guarantee segregated custody.

YouHodler operates at up to 90% LTV — the maximum in the retail market — and represents the highest-risk position on the custodial vs non-custodial spectrum: fully custodial with active rehypothecation exposure. At 90% entry LTV, a price decline of as little as 4–5% triggers a margin call. Combined with rehypothecation, this structure maximises two independent failure modes simultaneously: market-driven LTV breach and custody-chain collapse.

For a full platform-by-platform breakdown of LTV ranges, custody models, and liquidation mechanics, see BetterLending’s crypto lending platform comparison guide.

Three Custody-Related Mistakes That Amplify Loan Risk

1. Not Researching the Custodial vs Non-Custodial Structure Before Deposit

Borrowers who evaluate a loan on rate and LTV alone, without confirming custody structure, are accepting an unknown number of failure modes. Custody determines whether liquidation can execute cleanly, whether collateral is protected in insolvency, and whether rehypothecation risk exists. None of these are visible in the rate sheet. The time to confirm them is before deposit — not after a platform suspension notice.

2. High LTV Entry Without Understanding the Liquidation Trigger

Entering at 70%+ LTV on a platform with automated liquidation at 88% leaves an 18-percentage-point gap — equivalent to roughly a 20% further BTC price decline from entry. In a platform where liquidation executes automatically within hours of threshold breach, that gap can close during a single trading session. Borrowers who enter at high LTV without a liquid reserve and a personal action threshold at 65% or below are structurally exposed to automated liquidation with no recovery window.

3. No Reserve Liquidity for Collateral Top-Ups

The functional premise of a crypto-backed loan is liquidity access without forced asset sale. That premise requires 10–15% of the loan principal to be held in liquid stablecoin or fiat — separately from the loan capital — ready to deploy as collateral when LTV approaches the personal action threshold. Borrowers who commit 100% of accessible capital to the loan position, leaving no reserve, face a binary choice at the margin call: accept liquidation or sell the position they borrowed against. Both outcomes eliminate the original purpose of the loan.

Related BetterLending Guides

Borrowers evaluating custody structure before entering a position can find platform-specific detail in BetterLending’s crypto collateral and custody framework guide, which covers the four custody variables — control, segregation, rehypothecation, and recovery rights — that determine the real risk profile of a loan.

For borrowers at the pre-application stage, the borrower checklist for crypto-backed loan applications covers custody confirmation, LTV stress modelling, and reserve planning before committing $50,000+ in collateral. The checklist is structured around the five questions every borrower should be able to answer before deposit: who controls the keys, can collateral be reused, what triggers liquidation, how fast does it execute, and whether the borrower can intervene.

The Decision That Determines the Outcome

Most competitor content explains what custody is. This is not the useful question. The useful question is: who can take the collateral, under what conditions, and without what approval? The answer — established at deposit, not at margin call — determines whether a crypto-backed loan fails through market movement, through platform failure, or survives both.

A position with segregated custody, no rehypothecation, 50–55% entry LTV, and 10–15% reserve liquidity has reduced the failure modes to one: a price correction large enough to breach the liquidation threshold before the borrower can add capital. That risk is manageable and historical. Everything else — custody failure, rehypothecation chain collapse, automated liquidation without notification — is avoidable through structural decisions made before deposit.

The collateral deposit is not the start of the loan. It is the end of the borrower’s ability to change the structural conditions under which the loan operates. Every custody and rehypothecation decision is made before that transaction confirms.

Confirming the custody structure before committing collateral?

BetterLending works with crypto holders with $50,000+ in collateral to structure loans with segregated custody, no rehypothecation, and LTV thresholds calibrated to actual drawdown history. Review current loan terms and start an application, or speak with a lending specialist to confirm the custody structure before the deposit transaction is made.

Frequently Asked Questions

What is the difference between custodial vs non-custodial crypto loans?

In a custodial loan, the lender controls the private keys to the collateral from deposit to repayment. This gives the platform unilateral authority to execute liquidation when LTV thresholds are breached — typically at 83–90% LTV — without requiring borrower approval. In a non-custodial model, a multi-signature structure means multiple parties must approve any transaction, including liquidation. This protects the borrower from unilateral platform action but prevents capital providers from accepting the arrangement at scale, which is why non-custodial loans are generally limited to small peer-to-peer volumes.

What happens to collateral between deposit and repayment?

In a segregated, non-rehypothecating custodial loan, your collateral sits in a platform-controlled wallet address, Keys are being LTV is monitored in real time against price feeds, and the collateral is used exclusively to secure the loan. In a rehypothecating custodial loan, the collateral may additionally be lent to third parties, posted as margin elsewhere, or locked into a yield strategy — exposing it to counterparty risk entirely separate from BTC or ETH price movement. The borrower’s dashboard shows the same LTV ratio in both cases; the custody structure behind it is not visible from the loan interface.

Why does segregated custody matter in a platform insolvency?

In a segregated custody model, each borrower’s collateral is held in a dedicated account legally ring-fenced from the platform’s operational funds and other borrowers’ assets. In insolvency, segregated collateral is identifiable and legally protected — it does not become part of the general bankruptcy estate. In a pooled model, all collateral sits in accounts the platform controls collectively. In insolvency, individual borrowers must file claims through legal proceedings rather than recovering their specific collateral directly. The 2022 lender collapses produced recovery timelines of 18–36 months for borrowers in pooled structures; segregated structures produced faster and more complete recoveries.

Can a borrower stop liquidation once the threshold is breached in a custodial model?

No. In a fully custodial model, liquidation executes automatically when the LTV crosses the liquidation threshold — typically 83–90%. The platform controls the private keys and does not require borrower approval to execute the sale. The borrower’s window to prevent liquidation is between the margin call (75–80% LTV) and the liquidation threshold. On platforms with automated liquidation engines, that window may be under six hours. On platforms with structured notification processes — like BetterLending — the notification window is defined and sufficient to act. Confirming the notification timeline before entering the loan is not optional risk management.

What LTV should a borrower target at entry to maintain a viable response window?

For BTC or ETH collateral, 50–55% entry LTV provides a 28–33% further price decline buffer before a margin call triggers on a platform with a 78% margin call threshold. Entering at 60% reduces that buffer to approximately 23%; entering at 70% reduces it to approximately 11%. The personal action threshold — the LTV level at which a borrower should add collateral without waiting for a platform notification — should be set at 65% or below, providing at least 13 percentage points of additional buffer before the formal margin call is issued.

Does BetterLending rehypothecate collateral?

No. BetterLending does not rehypothecate collateral under any loan product or market condition. Collateral is held in segregated custody and used exclusively to secure the borrower’s loan. The non-rehypothecation policy is stated explicitly in the loan agreement. Borrowers can confirm the specific clause and the named custodian before committing any collateral — the answer is provided directly, not qualified by product tier or jurisdiction.

BetterLending does not provide financial or tax advice. This article is for informational and educational purposes only. Consult a qualified financial or legal professional before making borrowing or collateral decisions.