Borrowing against Bitcoin is a form of overcollateralized lending where a borrower locks BTC as collateral to access liquidity without triggering a taxable sale. Anyone who wants to Borrow against bitcoinshould note that these loans typically operate within defined loan-to-value (LTV) ranges, margin call thresholds, and liquidation levels that determine risk exposure.

In 2026, Bitcoin-backed loans are widely used by investors to avoid taxable events, access stablecoins, and maintain market exposure but they also come with real risks like liquidation, custody loss, and rising LTV ratios.

This guide breaks down exactly how it works, how much you should borrow, and how to avoid losing your Bitcoin.

What Does It Mean to Borrow Against Bitcoin?

Simply put, to borrow against Bitcoin means using your Bitcoin as collateral to get a loan in cash or stablecoins. Instead of selling your BTC to raise funds, you lock it up with a lender as security for the loan. This setup allows you to keep your Bitcoin exposure while accessing liquidity—but it also introduces risks like liquidation, custody, and platform reliability.

Read more: Is Borrowing Against Bitcoin Safe?

The idea behind this is that your Bitcoin’s value backs the loan. If everything goes smoothly and you repay what you owe, you get your Bitcoin back. But if you fail to repay, the lender has the right to sell your collateral to recover their funds. This mechanism creates a balanced relationship between borrower and lender, giving you access to funds without liquidating your holdings.

How does a crypto-backed loan work?

A crypto-backed loan allows a borrower to use Bitcoin as collateral to access liquidity without selling the asset. The process consists of three stages: collateral deposit, loan issuance, and repayment.

1. Collateral deposit and custody

The borrower transfers Bitcoin to a segregated custody account managed by a regulated third-party custodian such as BitGo.

The collateral is held separately from the lender’s operational funds and is not rehypothecated, meaning it is not lent out or reused.

Control of the collateral is governed by predefined loan conditions, including repayment, margin calls, and liquidation thresholds.

2. Loan issuance and LTV structure

The lender issues a loan based on a predefined loan-to-value (LTV) ratio, typically ranging between 10% and 65% of the Bitcoin’s market value.

For example, depositing $10,000 in Bitcoin at a 30% LTV allows the borrower to receive a $3,000 loan in fiat currency or stablecoins.

This overcollateralization ensures the collateral exceeds the loan value, reducing lender risk and protecting against price volatility.

3. Repayment, margin calls, and collateral release

The borrower repays the loan principal plus interest according to the agreed terms.

If the value of the collateral declines and the LTV rises beyond predefined thresholds, the borrower may receive a margin call requiring additional collateral or partial repayment.

Once the loan is fully repaid, the Bitcoin collateral is released from custody and returned to the borrower. If obligations are not met, the lender may liquidate part or all of the collateral to recover the loan.

While this process is simple in theory, some platforms may have slightly different terms or requirements, so it’s important to understand each step carefully. For a detailed walkthrough of each step—from choosing a platform to receiving funds—see: For a detailed walkthrough of each step—from choosing a platform to receiving funds—see: Step-by-Step: How to Take a Loan Against Bitcoin

How collateral custody works

When you borrow against Bitcoin, how your collateral is stored and controlled is a critical factor in managing risk.

At BetterLending, Bitcoin collateral is held in segregated custody accounts, meaning each borrower’s assets are kept separate from the platform’s operational funds. This structure ensures that your collateral is not mixed with other assets and remains clearly allocated to your loan.

Collateral is secured through a regulated third-party custodian, providing institutional-grade storage and controlled access. This reduces counterparty risk by ensuring that asset movement follows predefined conditions such as repayment, margin calls, or liquidation events.

In addition, BetterLending does not rehypothecate collateral. This means your Bitcoin is not lent out, reused, or deployed into other financial activities while your loan is active. The collateral remains fully reserved and tied exclusively to your position.

Unlike some lending models where collateral may be reused to generate additional yield, BetterLending maintains full collateral segregation and reserve backing. This approach aligns with custody standards used by platforms such as Ledn and Nexo, where asset protection and transparency are key components of risk management.

Understanding Loan-to-Value (LTV) Ratio

Loan-to-Value (LTV) determines how much you can borrow relative to your Bitcoin.

For example:

- $100,000 BTC at 50% LTV = $50,000 loan

The higher your LTV:

- The more you borrow

- The higher your risk

If Bitcoin drops in price, your LTV increases—and if it reaches a certain level around 80-85%, your collateral can be liquidated automatically. Most experienced borrowers stay between 10%–30% LTV to avoid liquidation risk. Learn how to calculate your safe borrowing range: How Much Should You Borrow Against Your Bitcoin?

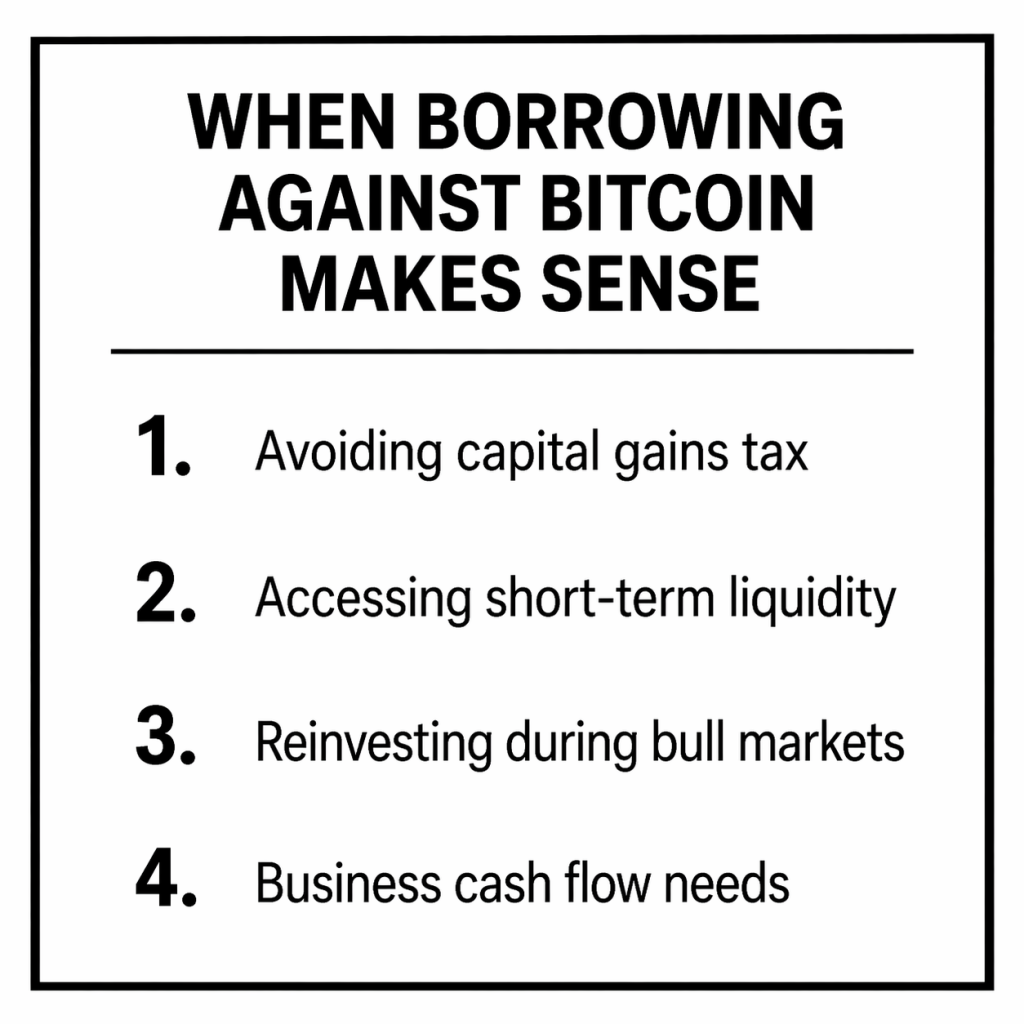

Why Do People Borrow Against Bitcoin Instead of Selling?

There are real-world reasons why Bitcoin holders might prefer borrow against bitcoin rather selling, even when they need cash. See real scenarios investors use in practice: Real Use Cases: Why People Take Bitcoin Loans Here are some common scenarios:

Accessing Liquidity Without Losing Exposure: Imagine you believe Bitcoin’s value will rise in the future but need funds now — maybe for personal expenses or investment opportunities. By borrowing against your Bitcoin, you keep your exposure to potential gains without liquidating your assets.

Avoiding Taxable Events: Selling Bitcoin may trigger capital gains taxes depending on your region. Borrowing against Bitcoin, on the other hand, generally isn’t a taxable event immediately, allowing you more flexibility in managing your tax situation.

Flexible Financial Planning: Bitcoin loans can be used for large purchases, consolidating debt, or covering short-term cash flow gaps. Borrowing this way offers financial flexibility while keeping your crypto portfolio intact.

Key Benefits of Borrowing Against Bitcoin

What Are The Key Risks Of Borrowing Against Bitcoin

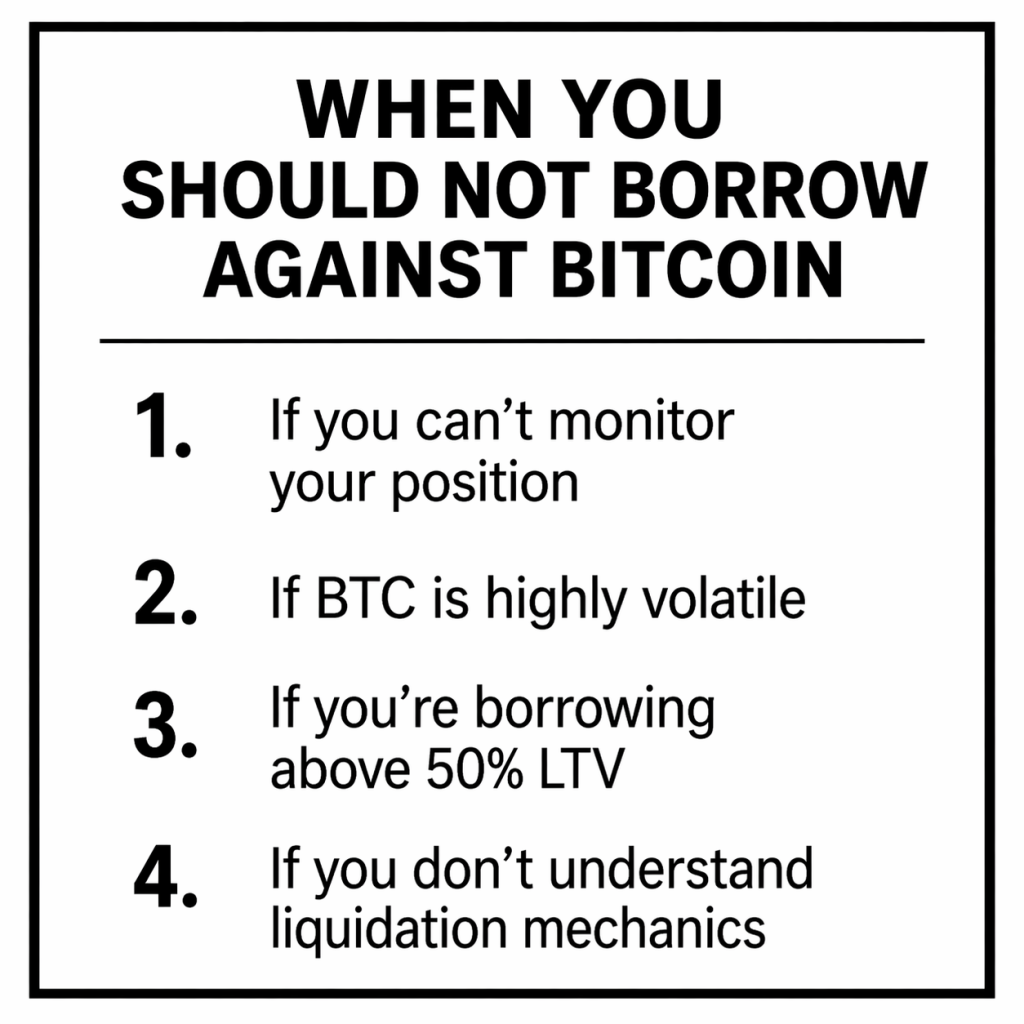

When you Borrow against Bitcoin you get introduced to three primary risk factors: loan-to-value (LTV) exposure, price volatility, and liquidation thresholds. These variables determine how much can be borrowed and how likely the collateral is to be liquidated under market stress.

1. Liquidation Risk

Liquidation risk happens when Bitcoin falls in value and your loan-to-value ratio rises too high. Once your LTV hits around 70-75% you will receive a margin call asking you to add collateral to avoid liquidation, But when LTV hits 80-85% the platform will liquidate or sell your BTC to recover the loan, this may happen before you have much time to react.

2. Custody Risk

Custody risk means you do not control the private keys to the Bitcoin used as collateral. at BetterLending.net, your collateral is kept in a segregated account this means if the platform is hacked, becomes insolvent, freezes withdrawals, or mismanages client assets, Your collateral will remain safe.

3. Interest Costs

Interest costs are the price you pay for borrowing against your Bitcoin, and they can range between 5-25%. Platforms like Betterlending.net offers standard interest rate of 9.99% for all loans, while Ledn offers around 9-11% interest rate depending on the amount of loan you want to take

4. Market Volatility

Bitcoin price swings can quickly turn a safe loan into a dangerous one.

How LTV, margin calls, and liquidation work in practice

A borrower deposits $100,000 worth of Bitcoin and takes a loan at a 50% LTV, receiving $50,000 in liquidity.

If the price of Bitcoin declines, the value of the collateral decreases, causing the LTV ratio to rise.

The lender may then sell part or all of the Bitcoin collateral to recover the outstanding loan balance.

If the collateral value drops to approximately $60,667, the LTV increases to 75%, triggering a margin call.

At this point, the borrower must either add more collateral or repay part of the loan to restore the LTV to a safe level.

If the collateral value continues to fall to around $50,882, the LTV reaches 85%, triggering liquidation.

Borrowing Against Bitcoin Offers Access to Funds Without Selling

In essence, when you borrow against Bitcoin it provides a way to tap into the value of your crypto holdings without selling them. By using your Bitcoin as collateral, you access liquidity, avoid immediate taxes, and maintain exposure to any future price gains. The process involves depositing your Bitcoin, receiving a loan based on a loan-to-value ratio, and repaying the loan to reclaim your assets.

While the benefits are significant, understanding key concepts such as volatility, liquidation risks, and loan terms is crucial for a safe, informed borrowing experience. For those interested in exploring Bitcoin loans, keeping risk awareness front and center is the smartest approach.

If you’re looking to borrow against Bitcoin with a structured and risk-aware approach, visit https://betterlending.net to learn more.

Frequently Asked Questions

- What does it mean to borrow against Bitcoin? It means using your Bitcoin as collateral to secure a loan without selling it. You lock up your BTC to get cash or stablecoins.

- How much can I borrow against my Bitcoin? Borrowing capacity is determined by the loan-to-value (LTV) ratio. For example, at a 50% LTV, depositing $100,000 in Bitcoin allows a borrower to access $50,000 in liquidity. Lower LTV ratios reduce liquidation risk, while higher LTV ratios increase exposure to margin calls.

- Is borrowing against Bitcoin safe? It can be safe if you understand the risks like price volatility and loan terms, and choose reputable lending platforms.

- What happens if Bitcoin drops in price during my loan? If your collateral value falls below a certain threshold, you may receive a margin call or face liquidation where your BTC is sold.

- Do I lose my Bitcoin when I take a loan? You temporarily transfer it to the lender as collateral, but you retain ownership unless you fail to repay.

- Are there tax consequences for Bitcoin loans? Borrowing typically isn’t a taxable event, unlike selling. However, consult a tax professional for advice tailored to your location.

- What can I use crypto-backed loans for? They’re flexible and can be used for anything—from investments to personal expenses or debt consolidation.

- How fast can I get a Bitcoin loan? Many platforms offer quick approval and funding, sometimes within 24-48 hours after collateral deposit.

- Can I repay the loan early? Yes, most lenders allow early repayment, which can reduce overall interest paid.

- What fees are involved? Expect interest rates and sometimes origination or maintenance fees; these vary by lender and loan terms.

- What’s the difference between unsecured loans and Bitcoin-backed loans? Bitcoin loans are collateralized, meaning they offer lower interest rates and easier approval because of the security you provide.

- How do I choose the right amount to borrow? It’s important to borrow within limits that won’t risk liquidation if Bitcoin’s price falls. Learning about how much you should borrow against Bitcoin helps manage this balance.