Borrowing against Bitcoin is a form of overcollateralized lending where a borrower uses BTC as collateral to access liquidity without selling the asset. These loans operate within defined parameters, including loan-to-value (LTV) ratios, margin call thresholds, liquidation levels, and why people take bitcoin loans which determine borrowing capacity and risk exposure. This structure allows Bitcoin holders to maintain market exposure while accessing cash or stablecoins.

How to Borrow Against Bitcoin Without Selling Your BTC

Borrowing against Bitcoin has become a popular way for holders to access liquidity without giving up their exposure to the coin’s future value. If you’ve ever asked yourself, “How can I unlock cash without selling my Bitcoin?” or “What are the real reasons behind Bitcoin loans?” then keep reading. We’ll walk through how it works, why it matters, and what you need to consider before getting started.

What Does It Mean to Borrow Against Bitcoin?

At its core, borrowing against Bitcoin means using your Bitcoin holdings as collateral to get a loan in traditional currency or stablecoins. Instead of selling your Bitcoin to raise funds, you pledge it to a lender—usually a crypto lending platform—in exchange for immediate cash or tokens. This way, you keep your Bitcoin in your wallet but still have access to liquidity.

Think of it as a mortgage on your home, except the asset you’re leveraging is cryptocurrency. The loan is secured by your Bitcoin, so if you repay as agreed, you get your Bitcoins back. If you don’t, the lender can claim them to recover the loan. Crypto-backed loans allow holders to stay invested in Bitcoin’s potential price increases, which is appealing in volatile markets or uncertain economic times. Understand risk before doing this: Is Borrowing Against Bitcoin Safe?

How does borrowing against Bitcoin work?

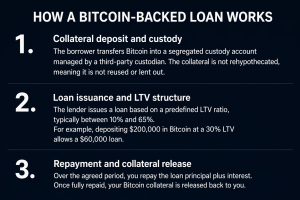

A Bitcoin-backed loan follows three core stages: collateral deposit, loan issuance, and repayment.

1. Collateral deposit and custody: The borrower transfers Bitcoin into a segregated custody account managed by a third-party custodian. The collateral is not rehypothecated, meaning it is not reused or lent out.

2. Loan issuance and LTV structure: The lender issues a loan based on a predefined LTV ratio, typically between 10% and 65%. For example, depositing $200,000 in Bitcoin at a 30% LTV allows a $60,000 loan.

3. Repayment and collateral release: Over the agreed period, you repay the loan principal plus interest. Once fully repaid, your Bitcoin collateral is released back to you.

Each step includes safeguards and terms that protect both lender and borrower, including how price volatility is handled if Bitcoin’s value changes dramatically.

Real Use Cases: Why People Take Bitcoin Loans in 2026

There are several real-world reasons why crypto holders prefer loans over outright sales. Let’s dig into the most common scenarios.

1. Holding Through a Bull Market While Accessing Cash:

A long-term holder believes Bitcoin will appreciate significantly over the next 2–3 years but needs liquidity today. Instead of selling and missing upside, they borrow at a low LTV (20–30%) and keep full exposure while accessing cash.

2. Avoiding Capital Gains Tax on Large Positions;

An investor sitting on significant unrealized gains wants to avoid triggering a taxable event. By borrowing instead of selling, they delay taxes while maintaining their position.

3. Using Bitcoin as Collateral for Business Liquidity;

A business owner holds BTC but needs working capital. Instead of selling long-term holdings, they use Bitcoin as collateral to fund operations while keeping exposure.

4. Taking Advantage of Market Opportunities;

An investor sees an opportunity (stocks, real estate, or crypto) but doesn’t want to sell BTC. Borrowing provides quick liquidity without exiting their core position. Learn how to borrow safely: How Much Should You Borrow Against Your Bitcoin

Key Benefits of Borrowing Against Bitcoin

- Maintain Market Exposure: Keep your Bitcoin even while accessing cash.

- Quick Access to Liquidity: Fast loan approval compared to traditional lending.

- Tax Advantages: Potentially avoid capital gains taxes associated with selling.

- Flexible Use: Use funds for anything, from investments to emergency expenses.

- Transparent Terms: Clear loan-to-value ratios and repayment structures make it easier to manage risk. See the full process: Step-by-Step: How to Take a Loan Against Bitcoin

Important Considerations Before Taking a Bitcoin Loan

While borrowing against Bitcoin offers advantages, it’s essential to understand the risks and loan mechanics involved.

Loan-to-Value Ratio (LTV): This percentage defines how much you can borrow relative to your Bitcoin collateral. Higher LTV increases borrowing power but reduces the buffer against price declines, increasing liquidation probability.

Market Volatility: Bitcoin prices can fluctuate significantly. If the value of your collateral drops too much, lenders may require additional collateral or initiate liquidation to cover the loan. Margin calls usually begin from 70-75% LTV

Liquidation Risk: If your collateral’s value falls below a certain threshold, usually at around 80-85% LTV the platform may sell your Bitcoin to recover the loan amount. This is why keeping an eye on market movements and your loan position is important.

Understanding what happens if Bitcoin drops in price and how to react can protect you from sudden losses and maintain your financial health.

Bitcoin loan structure and platform comparison

Bitcoin-backed loans are defined by key parameters that determine borrowing capacity and risk exposure. These include Bitcoin held as collateral in segregated custody, a typical loan-to-value (LTV) range of 10%–65%, a margin call threshold around 75%, and a liquidation level near 85%, which together define when action is required.

Crypto lending platforms follow similar overcollateralized models, but these parameters vary by provider. At BetterLending, loans operate within clearly defined LTV limits (10%–65%) with fixed margin call and liquidation thresholds, combined with segregated custody and a strict no rehypothecation policy.

Platforms like Ledn and Nexo also use overcollateralization, but differ in how they structure LTV ranges, custody models, and risk management systems. These differences directly impact borrower risk, transparency, and how collateral is handled during market volatility. See the full process: Step-by-Step: How to Take a Loan Against Bitcoin

If you’re looking to borrow against Bitcoin with a structured and risk-aware approach, visit Betterlending.net to learn more.

Frequently Asked Questions

- What does it mean to borrow against Bitcoin? It means using your Bitcoin as collateral to receive a loan in cash or stablecoins, allowing you to access funds without selling your crypto.

- How do Bitcoin loans work? You deposit Bitcoin as collateral, receive a loan based on the collateral’s value, repay the loan with interest, and then reclaim your Bitcoin.

- Why would I borrow against Bitcoin instead of selling it? Borrowing keeps you exposed to Bitcoin’s future price increases and may avoid triggering capital gains taxes from selling.

- What is Loan-to-Value (LTV)? LTV is the ratio of your loan amount to your collateral’s current value, indicating how much you can safely borrow.

- Are Bitcoin loans safe? Safety depends on the platform’s transparency, your attention to volatility, and your ability to manage repayments and collateral levels.

- What happens if Bitcoin’s price falls? If the price drops significantly, you might need to add collateral or face liquidation of the pledged Bitcoin.

- Can I use the loan for any purpose? Yes, once you receive the funds, you can use them for investments, expenses, or any other needs.

- Do I have to repay the loan in Bitcoin? Typically, loans are repaid in the currency you borrowed, such as USD or stablecoins, not in Bitcoin.

- How quickly can I get a Bitcoin-backed loan? Many platforms offer fast approval and funding, sometimes within hours or days.

- Is borrowing against Bitcoin taxable? The loan itself usually isn’t taxable, but tax laws vary, so consult your tax advisor.

- How do I choose how much to borrow? Consider your ability to repay and the LTV limits to reduce liquidation risks.

- Can I borrow against Bitcoin if I own a small amount? Some platforms have minimum collateral requirements, so it depends on your holdings and the lender’s policies.