Borrowing against Bitcoin is a form of overcollateralized lending where a borrower uses BTC as collateral to access liquidity without selling the asset. These loans operate within defined parameters such as loan-to-value (LTV) ratios, margin call thresholds, and liquidation levels, which determine borrowing capacity and risk exposure. If you’re a Bitcoin holder looking to access cash without selling your assets, borrowing against Bitcoin might have caught your interest. It offers a clever way to unlock liquidity without giving up your crypto position. But is borrowing against bitcoin safe? Learn How to Borrow Against Bitcoin Without Selling Your BTC IN 2026

This article dives into what borrowing against Bitcoin really means, how it works, and what you should keep in mind before taking the plunge.

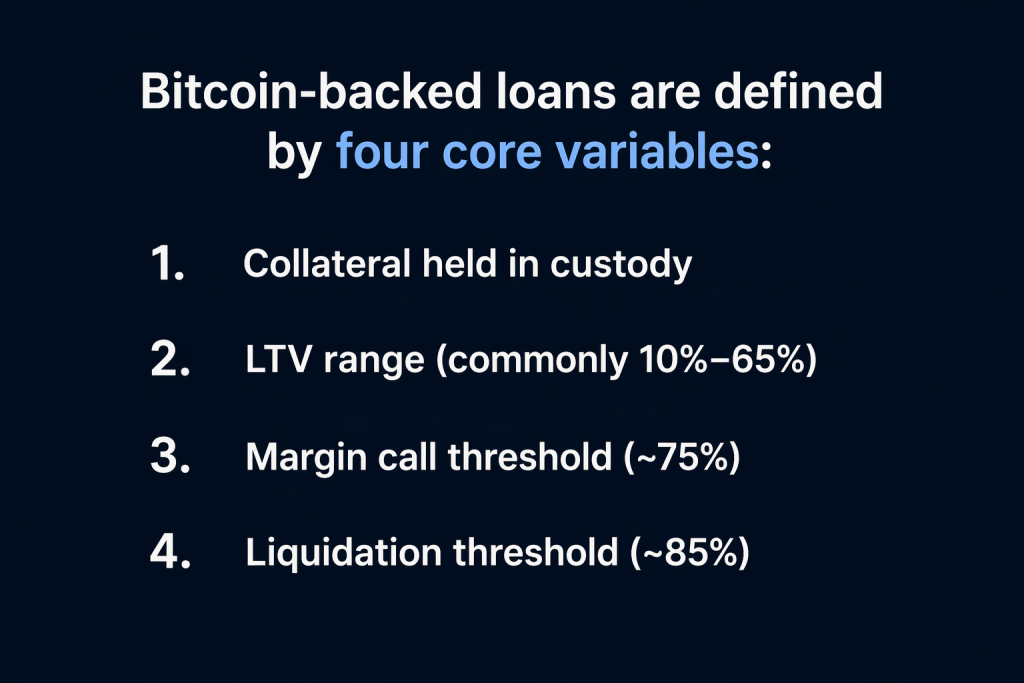

Bitcoin loan structure (key parameters)

Bitcoin-backed loans are defined by four core variables:

- Collateral held in custody

- LTV range (commonly 10%–65%)

- Margin call threshold (~75%)

- Liquidation threshold (~85%)

These parameters determine how much you can borrow and when corrective action or liquidation is triggered. See How Much Should You Borrow Against Your Bitcoin in 2026

What Does It Mean to Borrow Against Bitcoin?

Simply put, borrowing against Bitcoin means using your Bitcoin holdings as collateral to secure a loan. Instead of selling your Bitcoin to raise cash, you pledge it to a lender, who in return provides you with a loan, usually in fiat currency or a stablecoin. This arrangement lets you maintain ownership of your Bitcoin while freeing up funds for other purposes. It’s like putting your Bitcoin to work as security, so you don’t have to give it up when you need liquidity. Learn more

How does borrowing against Bitcoin work?

A Bitcoin-backed loan follows three core stages: collateral deposit, loan issuance, and repayment.

Collateral deposit and custody

Bitcoin is transferred into a custody system where it is held as collateral for the duration of the loan.

Loan issuance and LTV structure

Loans are issued based on a loan-to-value ratio, around 10-65% which determines borrowing capacity relative to collateral value.

Repayment and collateral release

The borrower repays the loan with interest usually ranges between 9-15%. Once repaid, the Bitcoin collateral is released. If LTV thresholds are exceeded, margin calls or liquidation may occur. Step-by-Step: How to Take a Loan Against Bitcoin in 2026

Keep in mind that during the loan term, fluctuations in Bitcoin’s price can affect the loan conditions, which is why understanding LTV and liquidation risks is crucial.

Why Do People Borrow Against Bitcoin Instead of Selling?

There are many practical reasons why Bitcoin holders opt for loans over a direct sale. Here are some common real-world scenarios:

Accessing Immediate Cash Flow: Perhaps you need to cover expenses or seize a timely investment opportunity but don’t want to part with your Bitcoin just yet.

Maintaining Market Exposure: Bitcoin has shown long-term growth despite volatility. Borrowing keeps your position intact, allowing you to benefit if prices recover or rise.

Tax Efficiency: In many regions, borrowing against crypto doesn’t trigger a taxable event like selling does. This can help defer taxable income and manage tax liability. Learn Real Use Cases: Why People Take Bitcoin Loans in 2026

Key Benefits of Borrowing Against Bitcoin

- Liquidity Without Selling: Unlock funds while retaining your Bitcoin holdings.

- Quick Access to Funds: Crypto-backed loans typically process faster than traditional loans.

- Flexible Repayment Options: Terms vary, allowing you to choose what fits your financial situation.

- Potential Tax Advantages: Preserve possible capital gains taxes by avoiding a sale.

- Use Funds for Any Purpose: There’s no restriction on how you use loan proceeds.

Important Considerations to Keep in Mind

While borrowing against Bitcoin offers many benefits, it comes with important risks and structural details to understand before proceeding:

Loan-to-Value (LTV) Ratio: This is the percentage of your Bitcoin’s value you can borrow. Higher LTV means more funds upfront but also greater risk of liquidation.

Volatility of Bitcoin: Bitcoin’s price can swing significantly. If the value drops below a certain threshold, lenders may liquidate your collateral to cover the loan.

Liquidation Risk: Failure to repay or sudden Bitcoin price drops can trigger forced sale of your collateral, meaning you could lose your Bitcoin.

Understanding how much you should borrow against Bitcoin and monitoring your loan terms can help you manage these risks effectively.

How BetterLending.net compares to other crypto lending platforms

Crypto lending platforms follow similar overcollateralized models, but structures differ across providers.

Platforms like Ledn and Nexo offer Bitcoin-backed loans with varying LTV ranges, custody models, and risk management systems.

Differences in these parameters directly affect borrower risk, transparency, and how collateral is handled during market volatility.

Exploring Related Questions

Many borrowers wonder about specific concerns like whether borrowing against Bitcoin is safe or what happens if Bitcoin drops in price. These topics are essential to research thoroughly before committing. Additionally, knowing how much you should borrow against Bitcoin can shape a responsible lending strategy that balances access to cash with risk tolerance.

Summary: Is Borrowing Against Bitcoin Safe?

Borrowing against Bitcoin can be a smart financial move when done with care and awareness. It allows you to unlock liquidity, keep your Bitcoin, and avoid selling during market dips. However, safety depends on understanding the loan structure, risks like volatility and liquidation, and choosing terms that suit your financial goals.

With clear knowledge and the right platform, borrowing against Bitcoin can offer convenience without sacrificing your position in the crypto market.

If you’re looking to borrow against Bitcoin with a structured and risk-aware approach, visit Betterlending.net to learn more.

Frequently Asked Questions

How does the borrowing process work with Bitcoin? You deposit your Bitcoin as collateral, receive a loan based on its value, then repay the loan to get your Bitcoin back.

What is loan-to-value (LTV)? LTV is the ratio of your loan amount to the value of your Bitcoin collateral, affecting how much you can borrow safely.

Is borrowing against Bitcoin safe? It can be safe if you understand the risks, especially volatility and liquidation, and choose reasonable loan terms.

What happens if Bitcoin’s price drops during my loan? If the price falls below a certain threshold, lenders may liquidate your collateral to cover the loan balance.

Can I borrow against Bitcoin without selling it? Yes, that’s the main advantage—accessing funds without selling your assets.

Are crypto-backed loans faster than traditional loans? Generally, yes. They use blockchain collateral and streamlined processes to speed up approval and funding.

Can I use the loan funds for any purpose? Most platforms allow you to use loan proceeds without restrictions.

Will borrowing against Bitcoin affect my taxes? Borrowing itself isn’t usually a taxable event, unlike selling Bitcoin, which may trigger capital gains tax.

What should I consider before borrowing against Bitcoin? Evaluate your ability to repay, understand LTV and liquidation risks, and monitor Bitcoin’s price movements.

Can I repay the loan early? Many lenders allow early repayment, which can reduce your interest costs.

What happens if I don’t repay the loan? The lender can liquidate your Bitcoin collateral to recover the loan amount.

How do I decide how much to borrow against Bitcoin? Assess your financial needs and risk tolerance, and borrow conservatively to avoid liquidation if Bitcoin’s price shifts downward.